Forward-Looking Returns

Many investors, amateurs and professionals alike, will build a portfolio based solely off of historical returns. In other words, their strategy is to simply buy what performed well in the past. While this can be profitable for short-term trading, long-term investing through the rearview mirror inevitably leads to disappointment.

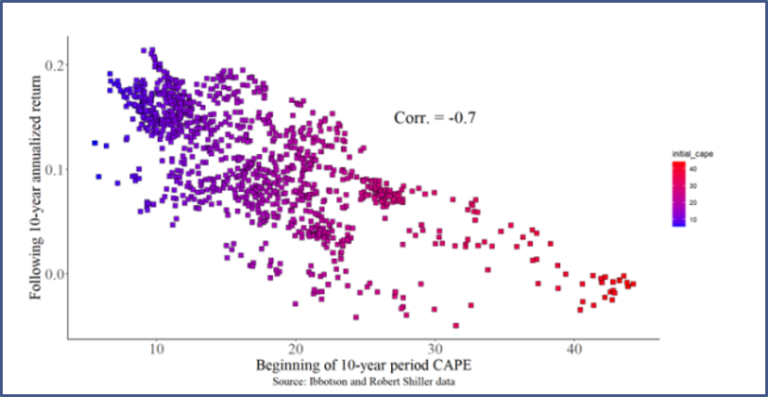

One simple example of the need for a forward-looking approach is the concept of valuations. We know higher valuation multiples are correlated with lower asset returns across stocks and bonds. Therefore, shouldn’t valuations be considered when building portfolios?

Beyond valuations, we recognize several other key drivers of returns from the research of Ibbotson, Grinold, and Kroner, including:

- Cash flow

- Earnings growth

- Inflation

- Buybacks/issuance

- Currency dynamics

- Default trends

We incorporate these to create return forecasts which we believe are reflective of today’s realities. Armed with this valuable information, we can now create an “efficient” portfolio, which is mathematically optimized to have the highest expected risk-adjusted return. Click here to learn more about efficient portfolios.